The US inventory market opened decrease on February 17, 2026. It’s the first session after Presidents’ Day, with the S&P 500 buying and selling round 6,840 at press time. The Index is down roughly 0.65% (round 44 factors) from Friday’s excessive, however up nearly 0.58% since at the moment’s open. This hints at consumers stepping in throughout sectors.

Persistent “SaaSpocalypse” fears that AI will disrupt conventional software program and tech fashions proceed to strain the market. This makes Info Expertise the weakest sector, down 1.5% intraday. Synopsys, Inc. (SNPS) leads the highest laggards, falling 1.6% amid broader AI nervousness.

High US Inventory Market Information:

• Empire State Manufacturing Index: The New York Fed’s survey confirmed modest regional growth in February at +7.1. It’s barely beneath January’s +7.7 however above forecasts. This main gauge for US manufacturing facility exercise affords some reassurance in opposition to slowdown fears.

• Canadian CPI Cools: January headline inflation eased to 2.3% YoY (from 2.4%), pushed by decrease gasoline costs. The softer print strengthens the disinflation narrative and will preview related tendencies in US knowledge, supporting Fed rate-cut hopes.

Sponsored

Sponsored

• US-Iran Oblique Talks Resume: Discussions in Geneva at the moment targeted on nuclear points and de-escalation. Progress might assist stabilize oil markets and cut back volatility within the power and world commerce sectors.

S&P 500 Exams Key Degree As AI Disruption Fears Weigh on Wall Road

Wall Road stays cautious on February 17, 2026, with the US inventory market buying and selling combined however total subdued amid persistent SaaSpocalypse fears. The S&P 500 opened weaker, briefly dipping beneath its 100-day EMA earlier than reclaiming it.

The index stabilized round 6,834–6,841 mid-session, down 0.65% intraday from its February 13 excessive.

The pattern suggests the market would possibly recuperate mildly, however the important thing to a broader restoration lies above the highs set on February 13 (Friday).

This echoes the late-November 2025 state of affairs. The index misplaced the 100-day EMA on November 28 however reclaimed it rapidly the following session, triggering a powerful rally. The S&P 500 gained roughly 7.38% from late November into late January.

The 100-day EMA has acted as sturdy help since then. Key help now sits round this zone, at round 6,819. An in depth beneath might invite broader weak spot towards 6,762 and 6,705. A decisive push above 6,889 (above Friday’s excessive) might goal the psychological 7,000 stage.

Nonetheless, stagflation-like issues (sticky inflation, development slowdown) and AI disruption nervousness restrict upside conviction.

Sponsored

Sponsored

Nasdaq Composite trades deeper within the crimson, highlighting tech’s drag. Tech’s 33% S&P 500 weight amplifies the affect on the broader index.

VIX, the Volatility Index, eased 1.08% to twenty.97 (from larger early-session ranges), signaling diminished volatility because the day progressed, although nonetheless elevated relative to current lows and reflecting warning.

The US 10-year Treasury yield is 4.05% (down modestly at the moment, close to 2.5-month lows).

It displays flight-to-safety flows and softer inflation expectations; supportive for bonds however pressuring development shares and crypto amid delayed rate-cut bets.

Sponsored

Sponsored

Sector Rotation in Focus: Defensives Shine Whereas Tech Drags

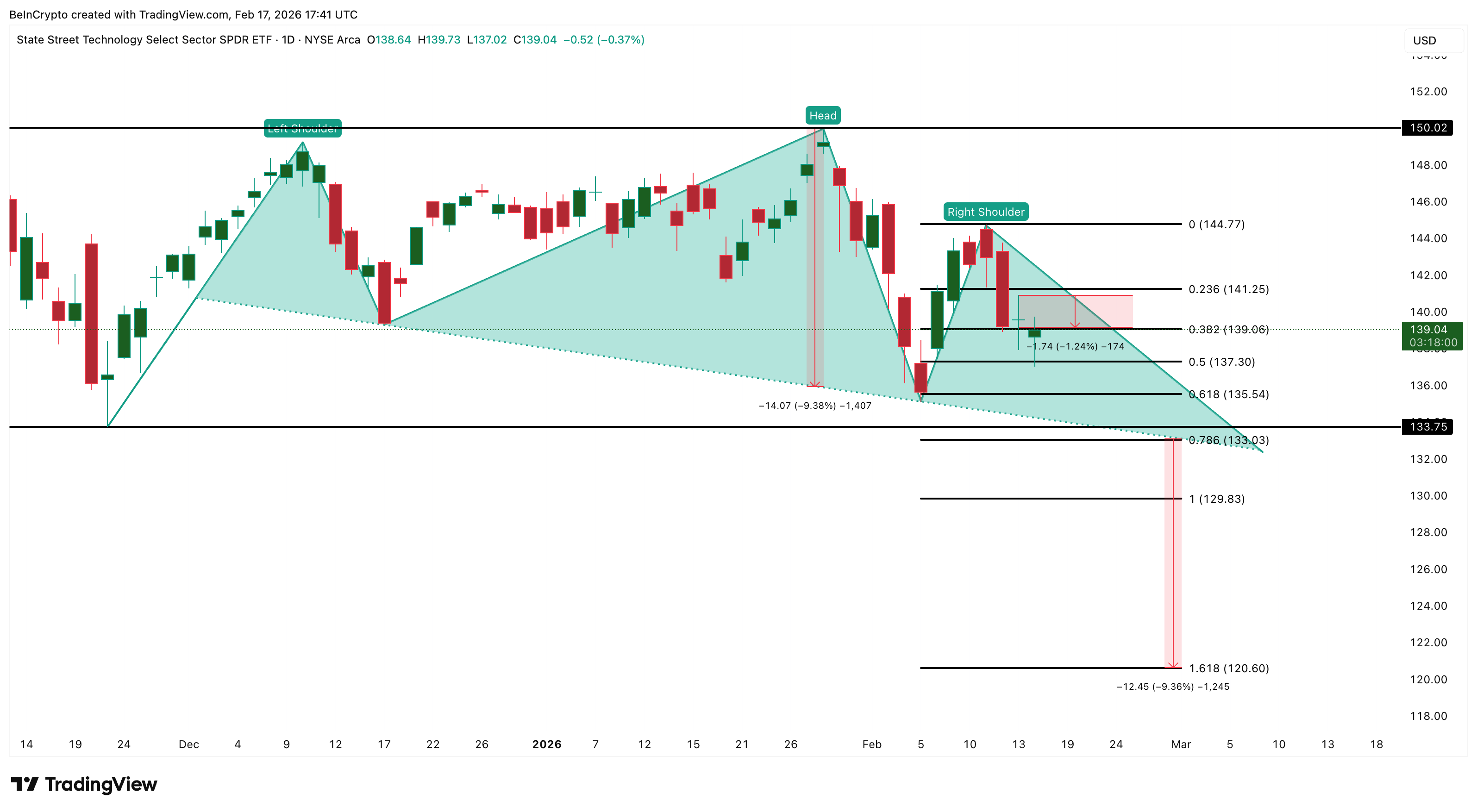

The US inventory market’s combined tone on February 17, 2026, reveals pronounced sector rotation. Expertise (XLK) is the standout laggard, down roughly 1.24% from February 13 highs (presently buying and selling -0.37% on the day).

XLK is the Expertise Choose Sector SPDR Fund, managed by State Road International Advisors, one of many flagship sector ETFs that slices the S&P 500 into its 11 GICS sectors for focused publicity.

It tracks main tech names (Nvidia, Microsoft, Apple) and software program/semiconductor firms. This makes XLK delicate to development sentiment and AI-related developments.

The XLK chart exhibits a growing head-and-shoulders sample, a bearish construction. The neckline holds regular close to 133; a decisive break beneath might affirm the sample and set off a ten% draw back transfer (measured from head to neckline), probably pushing towards 129 and even 120 in a deeper correction if broader market situations or AI issues worsen.

Utilities (XLU) continues to point out relative power after rallying 2.5% on Friday. Whereas it’s down 0.40% at the moment in step with broader weak spot, the sector stays the strongest performer on a weekly foundation.

This stream, from development/tech into defensives and worth, explains why the S&P 500 can commerce flat-to-lower regardless of inexperienced pockets: tech’s 33% index weight magnifies XLK weak spot, overshadowing positive aspects elsewhere.

Sponsored

Sponsored

The bearish setup invalidates on a reclaim of 141–144; a transfer above 150 would totally negate the menace.

Synopsys (SNPS) Drops 4.4% As AI Nervousness Hammers Software program Shares

Synopsys (SNPS) is likely one of the standout US inventory market laggards. It’s buying and selling at roughly 419 after dropping 4.43% intraday, at press time.

As a number one EDA software program and semiconductor IP supplier, SNPS is carefully tied to the software program infrastructure subsector. This leaves it susceptible to ongoing issues that AI might reshape chip-design workflows.

Within the Expertise Choose Sector SPDR Fund (XLK), SNPS carries a modest weight of 0.72%. This limits its direct ETF affect however serves as a powerful proxy for software program weak spot (e.g., ORCL -3.85%, CRWD -5.12%, FTNT -4.11%).

The every day chart exhibits SNPS buying and selling inside a bear flag sample following a 24% correction that started January 12, 2026, with the February 4 rebound/consolidation conserving worth contained inside the flag. It tried a breakdown at the moment, however consumers defended up to now.

A confirmed break beneath 416 might activate the sample, projecting draw back towards 322 (over 20% from present ranges). Intermediate help ranges sit at 402 and 371.

The bearish setup invalidates on a reclaim of 451. This reinforces rotation away from software program/development names into defensives, including to Nasdaq’s relative strain.