Bitcoin is transferring deeper into US family finance as homebuyers squeezed by excessive borrowing prices and restricted provide search for new methods to fund a down fee with out promoting their digital property.

On March 26, Higher Residence & Finance and Coinbase launched a construction that lets eligible debtors pledge Bitcoin or USD Coin (USDC) stablecoin to safe a separate mortgage for a down fee whereas nonetheless taking out a normal conforming mortgage on the house.

The association brings crypto into some of the intently watched components of the U.S. credit score system at a time when affordability pressures are already reshaping who can purchase a home and when.

The timing is central to the pitch as Realtor.com’s 2026 report put the US housing provide hole at 4.03 million properties.

This comes as the common 30-year mortgage price not too long ago climbed to 7%, whereas complete mortgage functions fell 10.5%, and buy functions dropped 5.4%. On the identical time, first-time patrons accounted for simply 21% of the market within the newest Nationwide Affiliation of Realtors profile.

In opposition to that backdrop, lenders and crypto corporations are betting {that a} rising class of would-be patrons has wealth in digital property however lacks the money liquidity wanted to clear one of many greatest limitations to homeownership.

A brand new route into the mortgage market

The Coinbase-backed product is aimed toward debtors who wish to retain publicity to crypto markets as an alternative of liquidating holdings to lift money for a down fee.

For a lot of, that call is about greater than market timing. Promoting crypto can even set off a tax invoice and power traders to cut back positions they view as long-term holdings.

Contemplating this, the construction is constructed round two loans at closing. The primary is a normal mortgage on the property. The second is a privately financed mortgage secured by pledged crypto and used to fund the money down fee.

Higher says the 15-year and 30-year fastened mortgage choices might be accessible, topic to credit score approval, and that the loans are designed in accordance with Fannie Mae tips in order that the mortgage stays a conforming mortgage.

That distinction is vital. The product doesn’t exchange the normal mortgage with a crypto mortgage. As a substitute, it wraps a crypto-secured financing layer across the down fee whereas leaving the principle mortgage in a traditional format.

For debtors utilizing Bitcoin, the preliminary collateral worth have to be a minimum of 250% of the mortgage quantity in fiat. For debtors utilizing USDC, the preliminary collateral worth have to be a minimum of 125%.

In sensible phrases, a borrower may pledge $250,000 in Bitcoin to unlock a $100,000 cash-down-payment mortgage, or $125,000 in USDC for a similar consequence.

The businesses are selling the association as a method to protect possession of digital property whereas having access to the housing market. Higher says each loans can share the identical rate of interest and amortization time period, making a single mixed month-to-month fee.

Housing pressure creates a gap

The product’s attraction is tied on to a housing market that has turn out to be more durable to enter, particularly for youthful patrons.

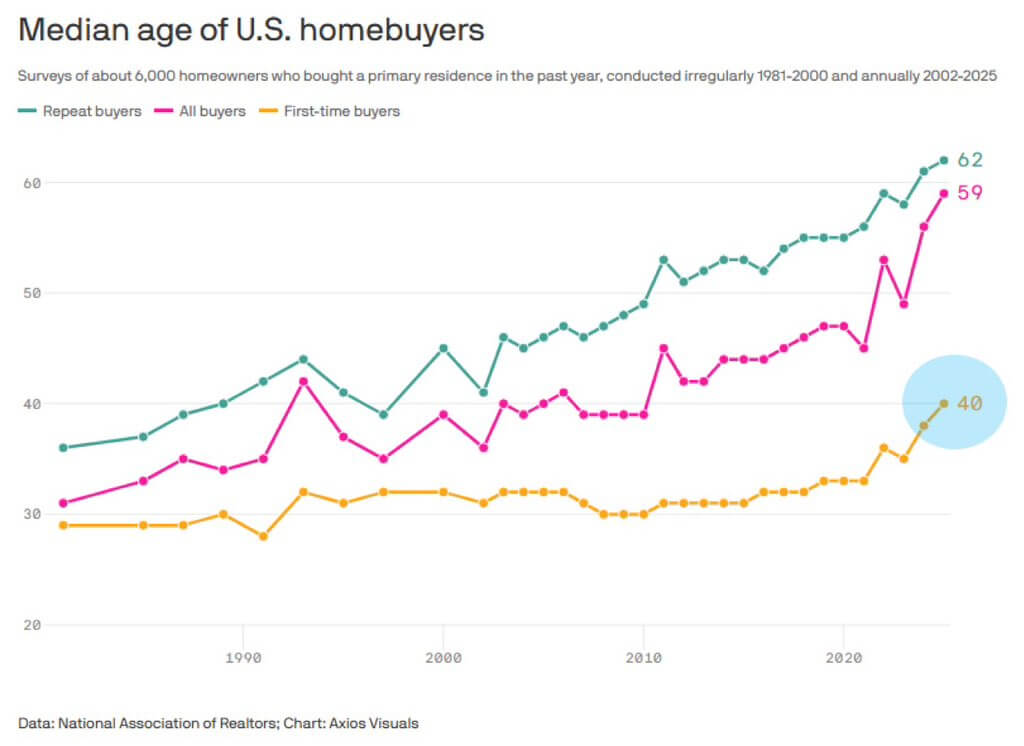

The median age of a first-time homebuyer reached 40 in 2025, in accordance with the Nationwide Affiliation of Realtors, reflecting the mixed impact of excessive mortgage charges, elevated residence costs, and restricted stock.

The strain is much more extreme for households decrease on the revenue scale. The NAHB/Wells Fargo Price of Housing Index for the second quarter of 2025 confirmed {that a} typical household wanted 36% of its revenue for a mortgage fee on a median new residence. For lower-income households, that share rose above 71%.

These figures assist clarify why firms see a possibility in linking digital property to housing finance. Conventional underwriting depends closely on documented revenue, credit score historical past, and money reserves.

That framework tends to favor households which have already constructed wealth by way of residence fairness, rising incomes, or long-established monetary property.

On the identical time, tens of millions of People have constructed positions in crypto. For context, round 20% of US adults, equal to 52 million folks, maintain some type of crypto asset, and nearly all of them are younger.

The NCA 2025 State of Crypto Holders report confirmed that 67% of token holders are 45 or youthful, and 26% earn lower than $75,000 a 12 months.

That provides the product a transparent goal market: youthful patrons with significant crypto publicity however restricted willingness, or means, to transform these holdings into money on the level of buy.

How the crypto pledge works

The businesses have tried to construction the product to look much less like a unstable crypto mortgage and extra like a mortgage-compatible financing instrument.

Debtors who pledge Bitcoin or USDC are usually not topic to margin calls or top-up necessities if the market worth of their collateral falls.

Higher says market actions alone don’t set off liquidation. As a substitute, the pledged property are solely in danger if a borrower turns into 60 days delinquent on funds, a threshold the businesses say mirrors the remedy of fee stress in conforming mortgages.

The crypto is held in custody for the lifetime of the down fee mortgage and returned as soon as that obligation is repaid. Debtors can not commerce the pledged property whereas they’re locked up, which preserves possession however restricts flexibility.

For USDC debtors, the stablecoin can proceed to earn rewards, which may assist offset mortgage servicing prices and cut back the borrower’s web efficient financing burden.

In the meantime, the broader ambition goes past one mortgage product. Higher and Coinbase say they intend, over time, to increase the vary of eligible digital property to incorporate tokenized equities, fastened revenue, and different tokenized actual property property.

This represents an indication that they see the mortgage providing as an early step in bringing on-chain wealth into mainstream client finance.

Coverage help and political resistance

In the meantime, this launch is arriving in a political local weather that has turn out to be extra receptive to crypto, however not with out resistance.

Fannie Mae’s position, together with oversight from the Federal Housing Finance Company, may assist make such merchandise extra mainstream than earlier crypto-linked mortgage choices.

Final 12 months, FHFA Director Invoice Pulte directed Fannie Mae and Freddie Mac to organize to depend crypto as an asset on mortgage functions, reflecting broader help for the digital-asset business from the Trump administration.

That coverage opening created room for industrial merchandise constructed round crypto wealth, but it surely additionally drew criticism from lawmakers who view the thought as a brand new supply of threat for housing finance.

Democratic senators, led by Elizabeth Warren, objected to the proposal, arguing that the present coverage doesn’t allow federally backed mortgage channels to think about cryptocurrency until it has first been transformed into US {dollars} and correctly documented.

They warned that increasing underwriting standards to incorporate unconverted crypto may introduce recent dangers to each the housing market and the broader monetary system.

That criticism goes to the center of the controversy round merchandise like Higher’s.

Supporters see them as a method to translate digital wealth into real-world entry with out forcing debtors to promote property and go away the market. Critics see a hazard in bringing a unstable and still-developing asset class nearer to the foundations of US residence lending.

So, the ultimate end result might depend upon whether or not crypto-backed mortgages stay a distinct segment instrument for prosperous digital-asset holders or evolve right into a broader financing channel for patrons shut out by the normal down fee hurdle.