The 12 months 2025 will probably be remembered because the second crypto futures buying and selling stopped being a theoretical threat and have become a measurable systemic failure. By 12 months’s finish, greater than $154 billion in compelled liquidations had been recorded throughout perpetual futures markets, in accordance with aggregated knowledge from Coinglass, translating to a mean of $400–500 million in day by day losses.

What unfolded throughout centralized and decentralized derivatives venues was not a single black swan occasion, however a slow-motion structural unwind.

Why Perpetual Futures Turned Liquidation Engines in 2025

The dimensions was unprecedented, with Coinglass’ 2025 crypto derivatives market annual report exhibiting $154.64 billion in complete liquidations for the previous 12 months.

But the mechanics behind the losses have been neither new nor unpredictable. All year long, leverage ratios elevated, funding charges issued persistent warnings, and exchange-level threat mechanisms proved to be deeply flawed beneath stress.

Sponsored

Sponsored

Retail merchants, drawn in by the promise of amplified positive factors, absorbed the majority of the injury.

The breaking level arrived on October 10–11, when a violent market reversal liquidated over $19 billion in positions inside 24 hours, the biggest single liquidation occasion in crypto historical past.

Lengthy positions have been disproportionately affected, accounting for an estimated 80–90% of liquidations, as cascading margin calls overwhelmed order books and insurance coverage funds alike.

Drawing from on-chain analytics, derivatives knowledge, and real-time dealer commentary on Twitter (now X), three core errors stand out. Every contributed on to the magnitude of losses witnessed in 2025, and every carries essential classes for 2026.

Mistake 1: Over-Reliance on Excessive Leverage

Leverage was the first accelerant behind 2025’s liquidation disaster and arguably the main crypto futures buying and selling mistake. Whereas futures markets are designed to reinforce capital effectivity, the dimensions of leverage deployed all year long crossed from strategic to destabilizing.

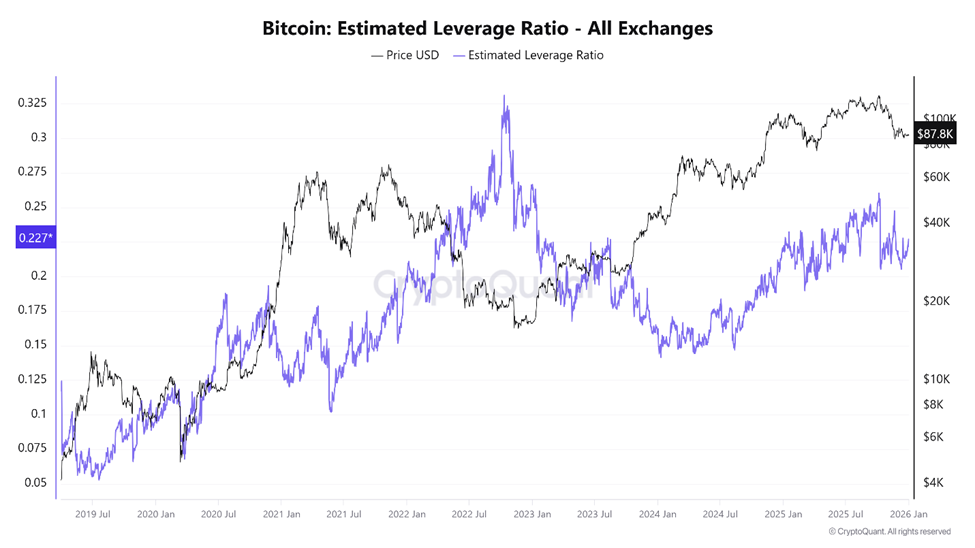

CryptoQuant knowledge signifies that the Bitcoin Estimated Leverage Ratio reached a document excessive in early October, simply days earlier than the market’s collapse.

On the similar time, complete futures open curiosity exceeded $220 billion, reflecting a market saturated with borrowed publicity.

On main centralized exchanges, estimated leverage ratios for BTC and ETH regularly surpassed 10x, with a significant portion of retail merchants working at 50x and even 100x.

“Excessive-leverage buying and selling is usually a double-edged sword…It gives a tantalizing alternative for revenue, however… can result in some fairly devastating losses,” OneSafe evaluation famous.

Coinglass knowledge from late 2025 illustrated the fragility of this construction. Whereas the long-to-short ratio remained close to equilibrium (roughly 50.33% lengthy versus 49.67% quick), a sudden worth transfer triggered a 97.88% surge in 24-hour liquidations, reaching $230 million in a single session.

Balanced positioning didn’t equate to stability. As a substitute, it meant each side have been equally overextended.

In the course of the October crash, liquidation knowledge revealed a brutal asymmetry. Lengthy positions have been systematically worn out as worth declines compelled market sells, pushing costs decrease and liquidating the following tier of leverage.

Sponsored

Sponsored

“In 2025, the on line casino facet of crypto lastly confirmed its true value. Greater than $150B in compelled liquidations vaporized leveraged futures positions… Most individuals should not buying and selling anymore; they’re feeding liquidation engines,” remarked one crypto researcher.

This was not hyperbole. Futures markets are mechanically designed to shut positions at predefined thresholds. When leverage is extreme, even modest volatility turns into deadly.

Liquidity evaporates exactly when it’s wanted most, and compelled promoting replaces discretionary decision-making.

Extreme Leverage Could Have Capped Crypto’s Bull Market

Some analysts argued that leverage did greater than wipe out merchants; it actively suppressed the broader market.

One thesis recommended that had the capital misplaced to compelled liquidations remained in spot markets, crypto’s complete market capitalization may have expanded towards $5–6 trillion, relatively than stalling close to $2 trillion. As a substitute, leverage-induced crashes repeatedly reset bullish momentum.

Leverage itself isn’t inherently damaging. Nevertheless, in a 24/7, globally fragmented, reflexive market, excessive leverage transforms futures venues into extraction mechanisms.

This tends to favor well-capitalized gamers over undercapitalized retail individuals.

Mistake 2: Ignoring Funding Fee Dynamics

Funding charges have been among the many most misunderstood and misused alerts in 2025’s derivatives markets. Designed to maintain perpetual futures costs anchored to identify markets, funding charges quietly convey essential details about market positioning.

When funding is constructive, longs pay shorts, signaling extra bullish demand. When funding turns unfavourable, shorts pay longs, reflecting bearish overcrowding.

In conventional futures markets, contract expiration naturally resolves these imbalances. Perpetuals, nevertheless, by no means expire. Funding is the one strain valve.

Sponsored

Sponsored

All through 2025, many merchants handled funding as an afterthought. Throughout prolonged bullish phases, the funding charges for BTC and ETH remained persistently constructive, slowly eroding lengthy positions via recurring funds.

Moderately than decoding this as a warning of crowding, merchants usually seen it as affirmation of development energy.

On-chain knowledge point out that DEX perpetual volumes reached a peak of over $1.2 trillion monthly, reflecting the explosive development in leverage utilization.

“…decentralized exchanges (DEXs) have been processing perp volumes of over US$1.2T monthly as of end-2025, with Hyperliquid nonetheless taking a big share of this market,” wrote David Younger, Coinbase International Head of Funding Analysis.

Hyperliquid accounted for the lion’s share of the DEX volumes. But few retail individuals adjusted positioning in response to funding extremes.

“The funding price isn’t an inefficiency. It’s the market telling you there’s an imbalance. If you accumulate funding, you’re being paid to offer liquidity—and to take actual threat,” wrote one dealer.

These dangers materialized violently. Sustained unfavourable funding episodes emerged as costs stabilized, signaling heavy quick positioning.

Traditionally, such situations have preceded sharp rallies. In 2025, they once more acted as gas for brief squeezes, punishing merchants who mistook unfavourable funding for directional certainty.

Compounding the problem, funding dynamics started to sync with DeFi lending markets in periods of volatility. As merchants borrowed spot belongings to hedge or quick futures, platforms like Aave and Compound noticed utilization charges spike above 90%, driving borrowing prices sharply increased.

The end result was a hidden suggestions loop: funding losses on perps paired with rising curiosity bills on borrowed collateral.

Sponsored

Sponsored

What many perceived as impartial or low-risk methods quietly bled capital from each side. Funding was not free cash. It was compensation for offering stability to an more and more unstable system.

Mistake 3: Over-Trusting ADL As a substitute of Utilizing Cease Losses

Auto-deleveraging (ADL) was the ultimate shock that many merchants have been unaware of till it worn out their positions.

ADL is designed as a last-resort mechanism, triggered when alternate insurance coverage funds are depleted, and liquidations go away residual losses. As a substitute of socializing these losses, ADL forcibly closes positions of worthwhile merchants to revive solvency. A mix of revenue and efficient leverage usually determines precedence.

In 2025, ADL was now not theoretical.

In the course of the October liquidation cascade, insurance coverage funds throughout a number of venues have been overwhelmed. Consequently, ADL triggered en masse, usually closing worthwhile shorts first, at the same time as broader market situations remained hostile. Merchants working hedged or pairs methods have been hit significantly onerous.

“Think about getting your quick closed first after which getting liquidated in your lengthy. Rekt,” wrote Nic Pucrin, CEO and co-founder of Coin Bureau, in response to the October crash.

ADL operates on the single-market stage, with out regard for portfolio-wide publicity. A dealer could seem extremely worthwhile on one instrument whereas being completely hedged throughout others. ADL ignores that context, breaking hedges and exposing accounts to bare threat.

Critics argue that ADL is a relic of early isolated-margin techniques and doesn’t scale to trendy cross-margin or options-based environments. Some exchanges, together with newer on-chain platforms, have explicitly rejected ADL in favor of socialized loss mechanisms, which defer and distribute losses conditionally relatively than crystallizing them immediately.

For retail merchants, the lesson was unequivocal. ADL isn’t a security web. It’s an exchange-level solvency device that prioritizes platform survival over particular person equity. With out strict, guide stop-losses, merchants have been uncovered to complete account wipeouts, no matter their leverage self-discipline.

Classes for 2026

Crypto derivatives will stay a dominant drive in 2026. Futures markets provide liquidity, worth discovery, and capital effectivity that spot markets can’t match. Nevertheless, the occasions of 2025 made one reality unavoidable: construction issues greater than conviction.

- Over-leverage transforms volatility into annihilation.

- Funding charges reveal crowding lengthy earlier than worth reacts.

- Change threat mechanisms are designed to guard platforms, not merchants.

The $154 billion misplaced in 2025 was not an accident. It was tuition paid for ignoring the mechanics of the market. Whether or not 2026 repeats the lesson will depend upon whether or not merchants lastly select to be taught it.