The primary week of 2026 supplied traders a distinctly unromantic reminder: when the macro narrative shifts from “development and inflation” to “institutional and governance danger”, efficiency is now not about whose story sounds greatest, however about which belongings look most unbiased underneath stress.

Gold and silver’s relative power, alongside the relative weak point of BTC and ETH, captures that repricing. Exhausting belongings are competing for an “independence premium”, whereas main cryptoassets are more and more buying and selling like high-volatility greenback danger. This isn’t to argue that crypto has misplaced its long-term case.

It’s that, within the present framework, the market is targeted on three questions: What do you agree in? Who’s the marginal purchaser? Which danger bucket do you sit in inside a portfolio? On these factors, the hole between treasured metals and crypto is widening.

USD-Denominated Leverage and “Institutional Threat”

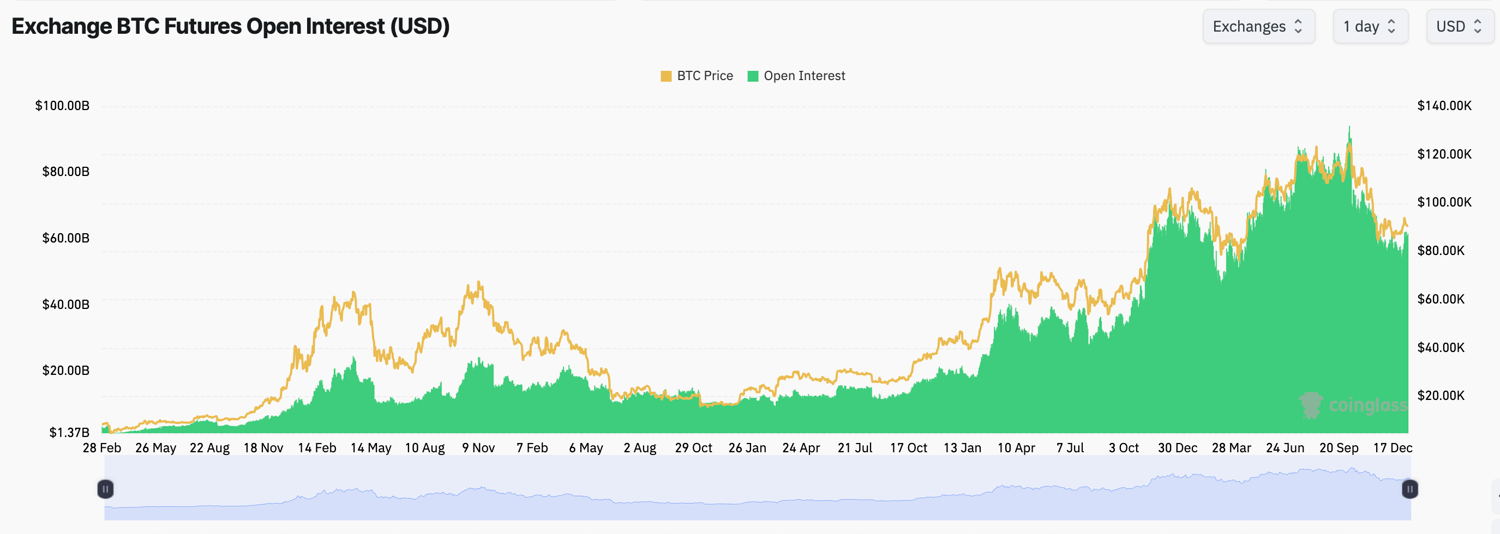

A fast look again at Bitcoin over the previous yr helps. Throughout final April’s “Liberation Day” rally, BTC stabilised first after which rebounded, printing a brand new excessive of $126k six months later. The “digital gold” narrative mattered, however the true afterburner was USD-settled derivatives.

From March to October 2025, open curiosity in BTC Delta 1 contracts jumped from about $46bn to greater than $92bn, giving BTC highly effective leverage assist and serving to it outperform gold within the quick run. After the height, a broad crypto deleveraging and shifting institutional expectations pushed BTC right into a sustained drawdown; gold, against this, saved grinding larger.

Supply: Tradingview

One element issues: as USDT/USDC and different stablecoins have develop into entrenched, USD-denominated leverage (not coin-margined leverage) has more and more pushed the marginal transfer.

As publicity is taken by extra standardised, extra levered channels—exchanges, perps, structured merchandise—behaviour turns into extra “portfolio-like”: add on risk-on, minimize as a part of a risk-budget discount.

Whether or not it’s USD pricing, USD collateral, or cross-asset hedging constructed across the US price curve, BTC is definitely folded into the identical USD-based danger framework. So when greenback liquidity tightens, regardless of the set off, BTC is usually among the many first to really feel the results of de-risking.

Put in a different way, the market hasn’t instantly “stopped believing” in digital gold. It’s more and more treating BTC as a tradable macro issue—nearer to high-volatility greenback beta than a retailer of worth outdoors the system.

What will get offered isn’t a lot spot BTC as USD-denominated BTC publicity. As soon as leverage turns into giant sufficient for flows to dominate fundamentals, BTC behaves like a basic danger asset, being delicate to liquidity, actual charges, and monetary coverage.

Gold is completely different—a minimum of for now. Its worth remains to be pushed primarily by spot provide and demand relatively than leverage. It additionally retains financial traits and is extensively accepted as collateral: a form of offshore onerous forex. That makes it one of many few belongings indirectly dictated by day-to-day fiscal and financial settings.

On this setting, that issues. The Trump administration has added to macro and coverage uncertainty (consider what occurred in Venezuela and Minnesota). For world traders, holding greenback belongings and greenback leverage now not seems like “parking the ship in a protected harbour”; even on the stage of pricing and settlement, it carries harder-to-model institutional danger that may problem the predictability of market guidelines.

Because of this, decreasing artificial publicity to US coverage danger is a smart transfer. Property extra tightly sure to the greenback system—and which behave like danger belongings in stress — are usually minimize first. Conversely, belongings which can be extra clearly indifferent from sovereign credit score and fewer depending on “permissioned” monetary infrastructure seem extra beneficial in the identical danger mannequin.

That’s a headwind for crypto and a tailwind for treasured metals: independence is the purpose. When markets concern shifting coverage boundaries and weaker rule predictability, gold (and different treasured metals) earns the next independence premium.

Since 2025, that premium has develop into extra seen. A neat comparability is silver versus ETH. Within the public creativeness, ETH was as soon as generally known as “digital silver” (and, within the PoW period, it arguably was). Each have been seen as smaller-cap belongings, extra liable to squeezes and leverage-driven strikes.

However ETH, an equity-like asset deeply tied to the greenback system, has lengthy since misplaced any independence premium. Silver, as one of many historic “offshore onerous currencies”, has not. Traders are clearly prepared to pay up for that independence.

The “Greenback Beta Low cost”

USD-denominated leverage can be a key motive choices markets stay structurally bearish on BTC and ETH. The “New 12 months impact” lifted each briefly within the first few periods, however it didn’t shift the longer-dated positioning.

Over the previous month, as traders have continued to cost rising institutional danger in greenback belongings, longer-dated bearishness in BTC and ETH has constructed additional. Till the share of USD leverage falls meaningfully, “independence underneath institutional uncertainty” is more likely to keep the market’s organising precept.

On the identical time, as valuation expectations for dollar-linked belongings are marked down, traders are demanding extra danger premia. The ten-year Treasury yield remains to be elevated at round 4.2%. With the Treasury and the Fed unable to totally dictate the pricing of 10-year length, that stage raises the hurdle price for danger belongings.

But the “greenback beta low cost” related to USD leverage compresses implied ahead returns for BTC and ETH (to five.06% and three.93%, respectively). BTC should look tolerable; ETH, a lot much less so. ETH subsequently wears a deeper greenback beta low cost: yields aren’t aggressive, and upside convexity is capped. None of this negates Ethereum’s long-term potential—however it does change allocation decisions over a one-year horizon.

Crypto can, in fact, bounce again: if monetary situations ease, coverage uncertainty fades, or the market pivots again to pricing development and liquidity, high-volatility belongings will naturally reply. However macro traders are targeted on taxonomy. When institutional uncertainty dominates, crypto trades like danger belongings; treasured metals commerce extra like “exceptionalism belongings”.

That’s the message for early 2026: crypto hasn’t “failed”—it has merely, for now, misplaced its pricing slot as an unbiased asset on this macro regime.

Disclaimer: The knowledge supplied herein doesn’t represent funding recommendation, monetary recommendation, buying and selling recommendation, or some other kind of recommendation, and shouldn’t be handled as such. All content material set out under is for informational functions solely.