For international buyers, 2025 was one of the vital undercurrent-filled years of the twenty first century. Not like the bursting of the dot-com bubble in 2001 or the worldwide monetary disaster in 2008, markets in 2025 didn’t expertise a protracted, large-scale liquidation cycle or a “storm-like” sequence of relentless crashes.

But it’s clear that, amid geopolitical uncertainty, uncertainty over US fiscal and financial coverage, uncertainty throughout a number of international locations’ financial fundamentals, and the ebbing of globalisation in favour of regionalisation, equities, bonds, commodities and crypto have all been pricing in a future that’s extra cautious and extra defensive.

In opposition to that backdrop, liquidity allocation has turn into much less concentrated in equities and bonds than it as soon as was. Commodities, FX and charges attracted larger consideration in 2025. On the identical time, buyers have been steadily lowering leverage and trimming publicity to higher-risk property—one of many direct causes the crypto bull market led to This fall 2025.

So, the place do markets go in 2026? As in 2025, implied expectations embedded in derivatives-market information have already provided a solution.

Liquidity: Not Plentiful

Initially of 2025, one main “bullish” think about buyers’ minds was Donald Trump’s formal inauguration. The prevailing view was that Trump would set off extra price cuts, inject extra liquidity into markets, and drive asset costs greater.

Certainly, between September and December 2025, amid “considerations a few weakening labour market”, the Federal Reserve delivered three “defensive” price cuts and, in December, introduced the tip of quantitative tightening. However this didn’t produce the liquidity flood buyers had hoped for.

From October 2025 onwards, the Efficient Federal Funds Price (EFFR) steadily moved in the direction of the midpoint of the “price hall”. Within the following months, EFFR crossed that midpoint and drifted in the direction of the higher sure of the hall—hardly an indication of simple liquidity.

EFFR is the core short-term market price within the US. It displays funding liquidity circumstances within the banking system and the way the Fed’s coverage stance (hikes or cuts) is transmitted in observe. In comparatively loose-liquidity regimes, EFFR tends to sit down nearer to the decrease finish of the hall, as banks have much less want for frequent in a single day borrowing.

Within the ultimate months of 2025, nonetheless, banks clearly confronted liquidity tightness—a key driver of the rise in EFFR.

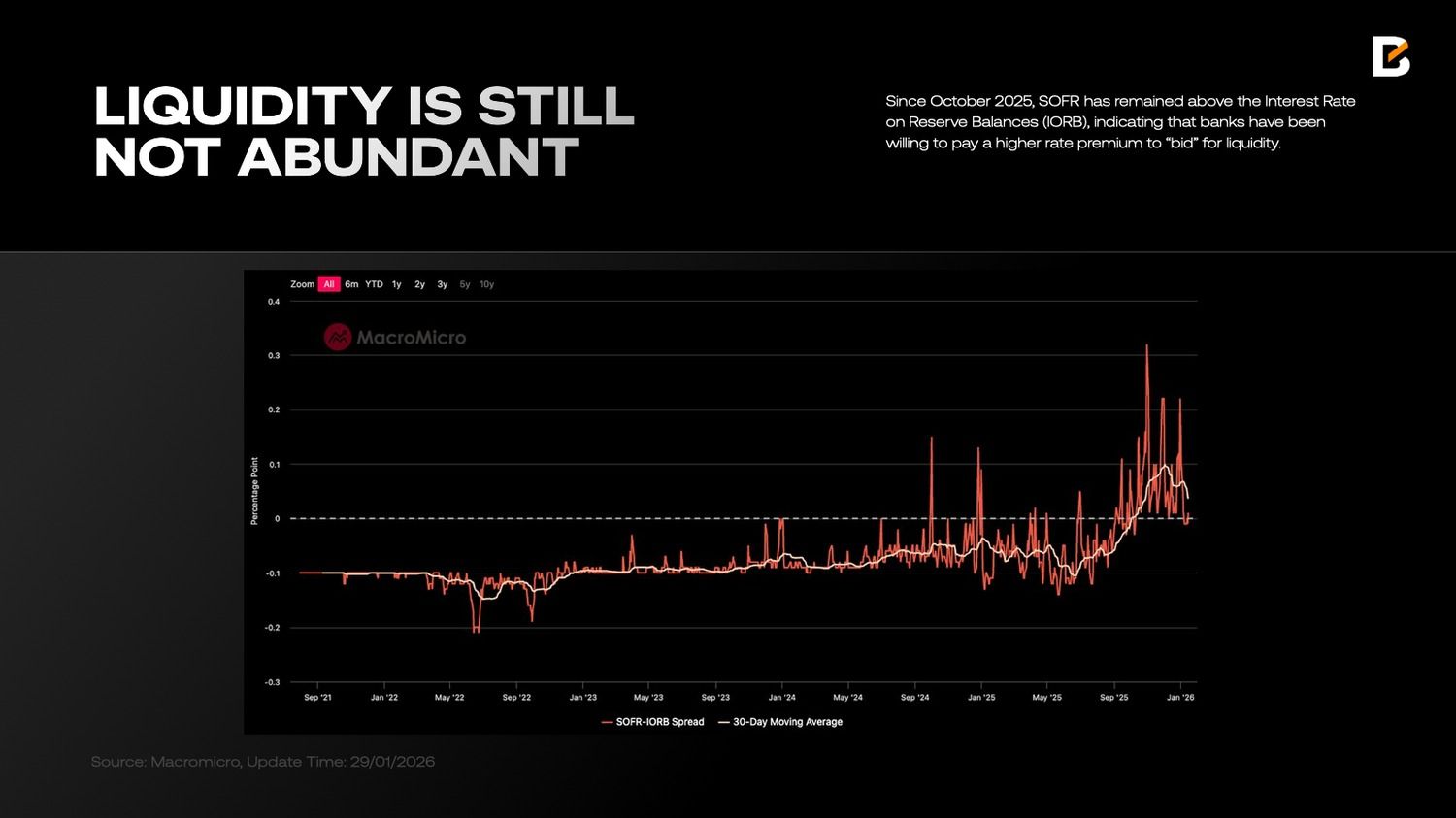

The SOFR–IORB unfold additional highlights the diploma of stress. If EFFR primarily displays cash-market circumstances, SOFR, secured funding collateralised by US Treasury securities, captures a broader liquidity scarcity. Since October 2025, SOFR has remained above the Curiosity Price on Reserve Balances (IORB), indicating that banks have been prepared to pay a better price premium to “bid” for liquidity.

Notably, even after the Fed stopped shrinking its stability sheet, the SOFR–IORB unfold didn’t fall sharply in January. One believable rationalization is that, throughout 2025, banks deployed a major share of their liquidity buffers into monetary investments somewhat than extending credit score to the business, industrial, and actual property sectors.

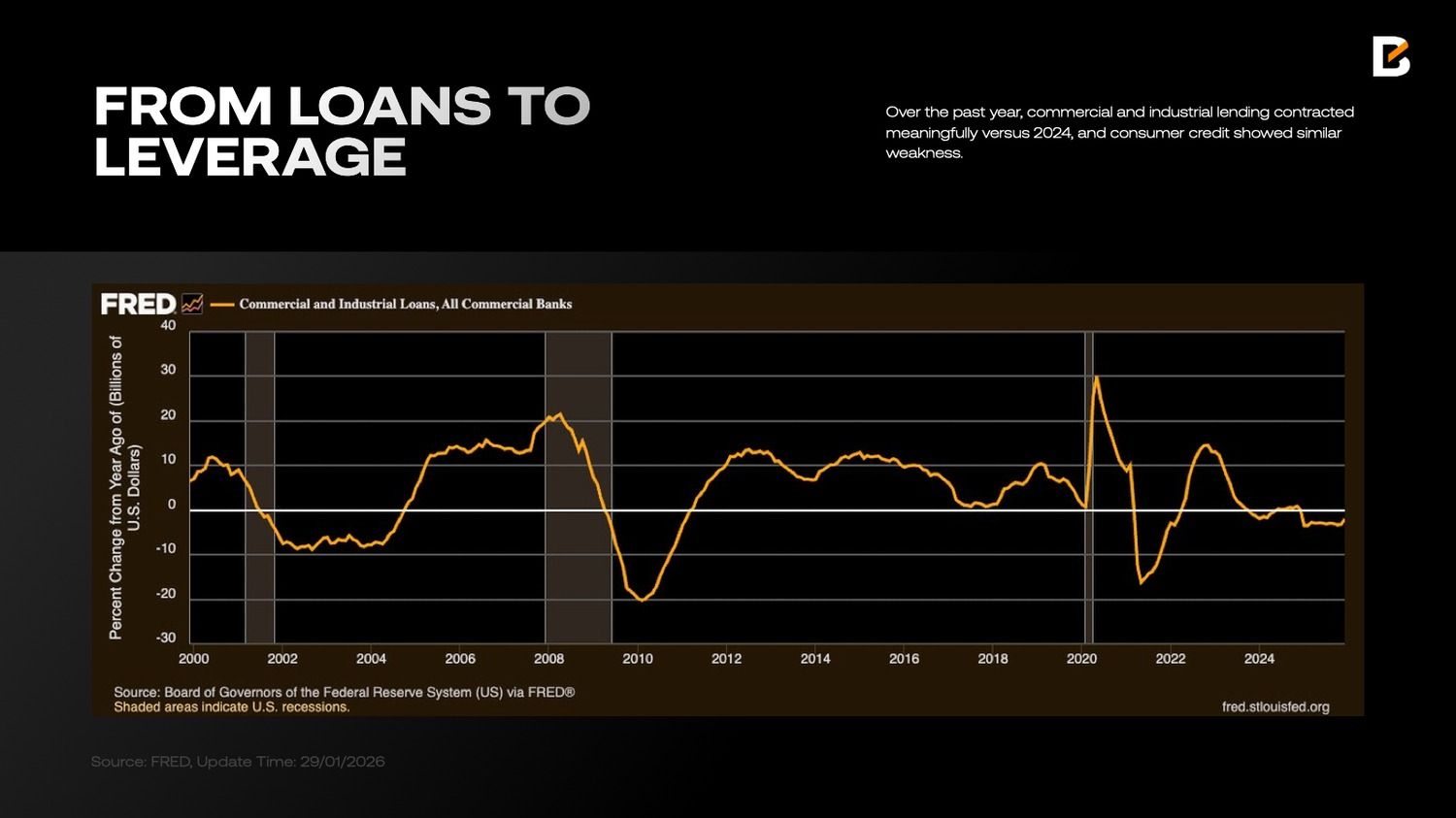

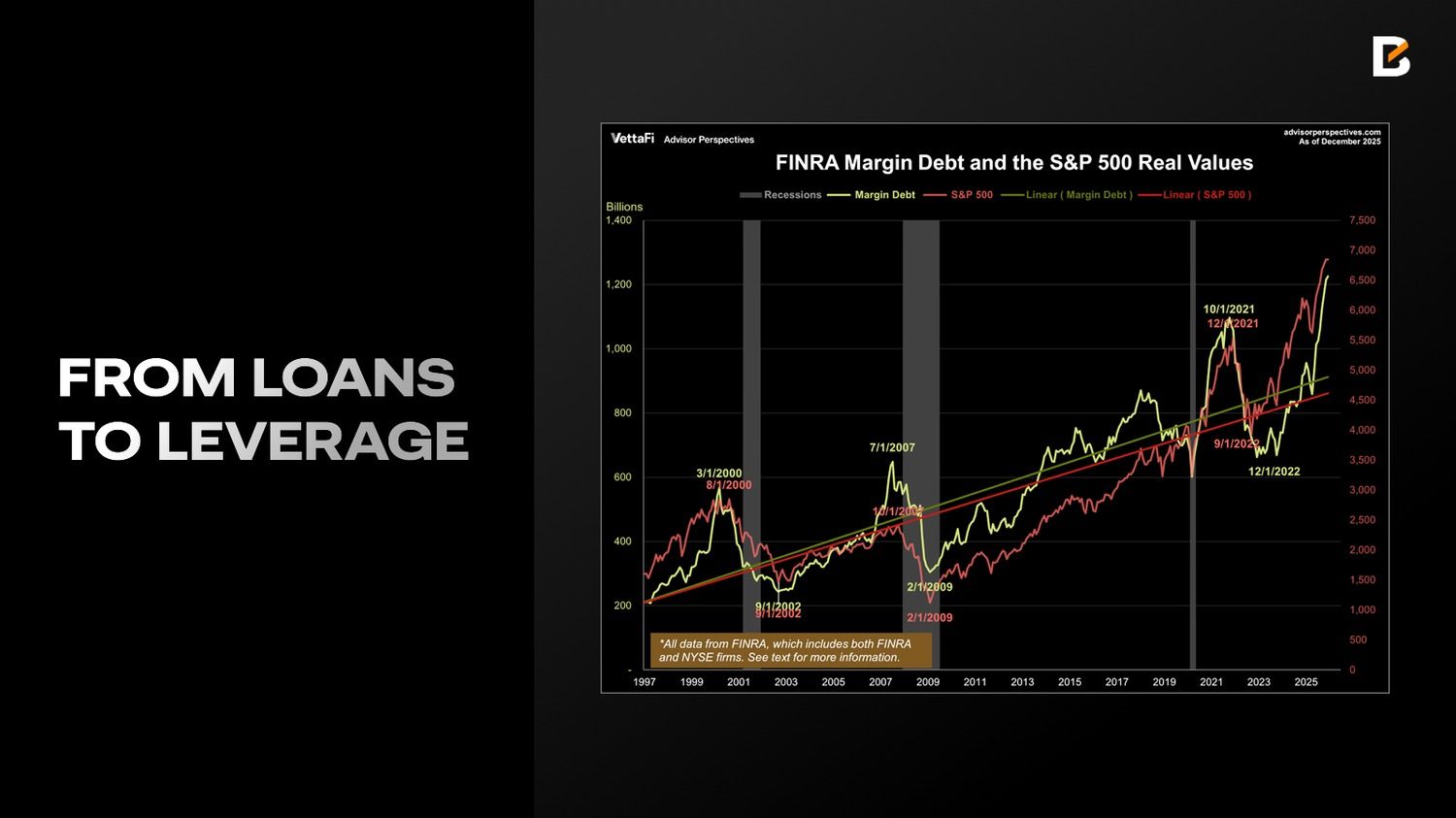

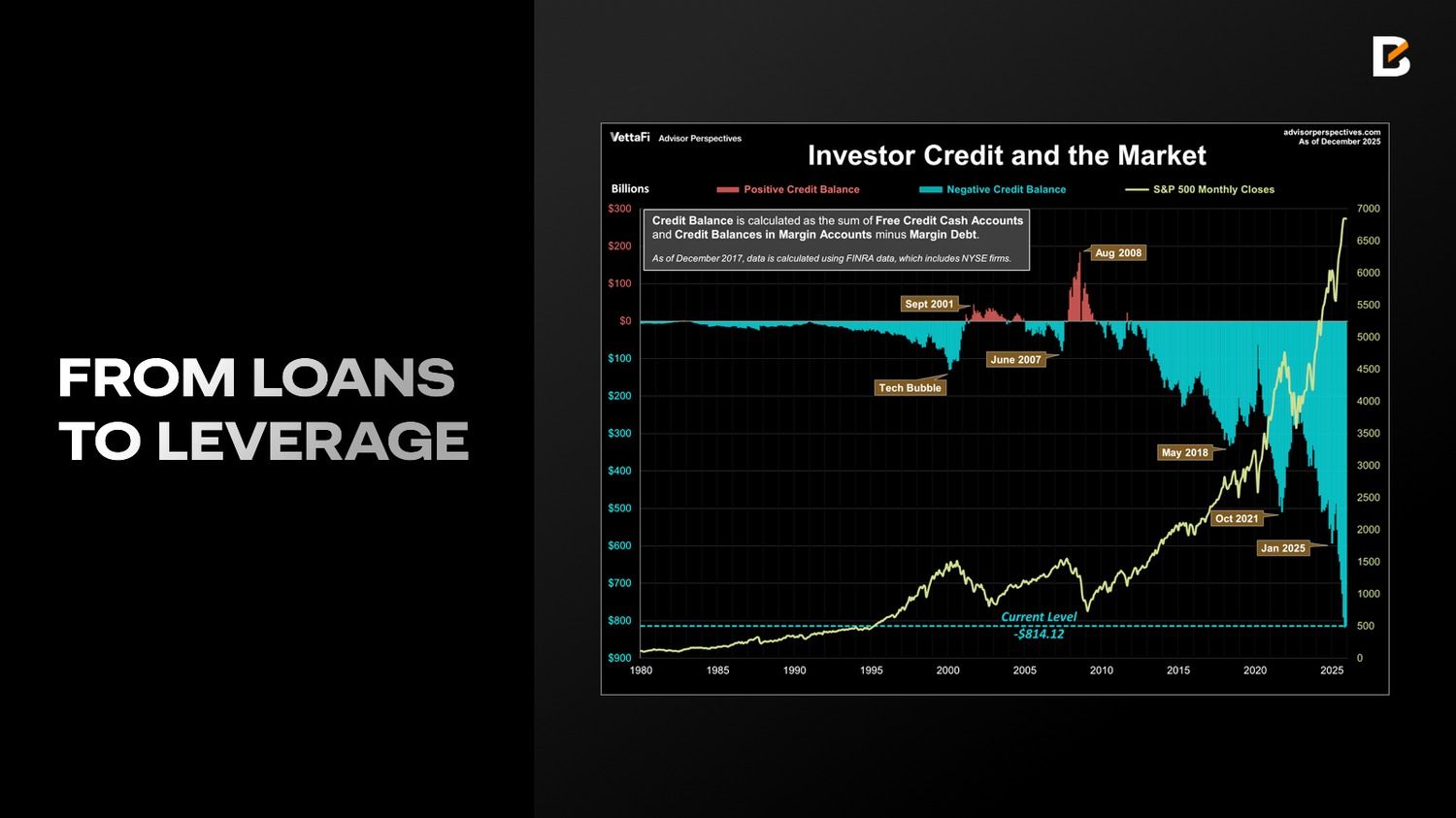

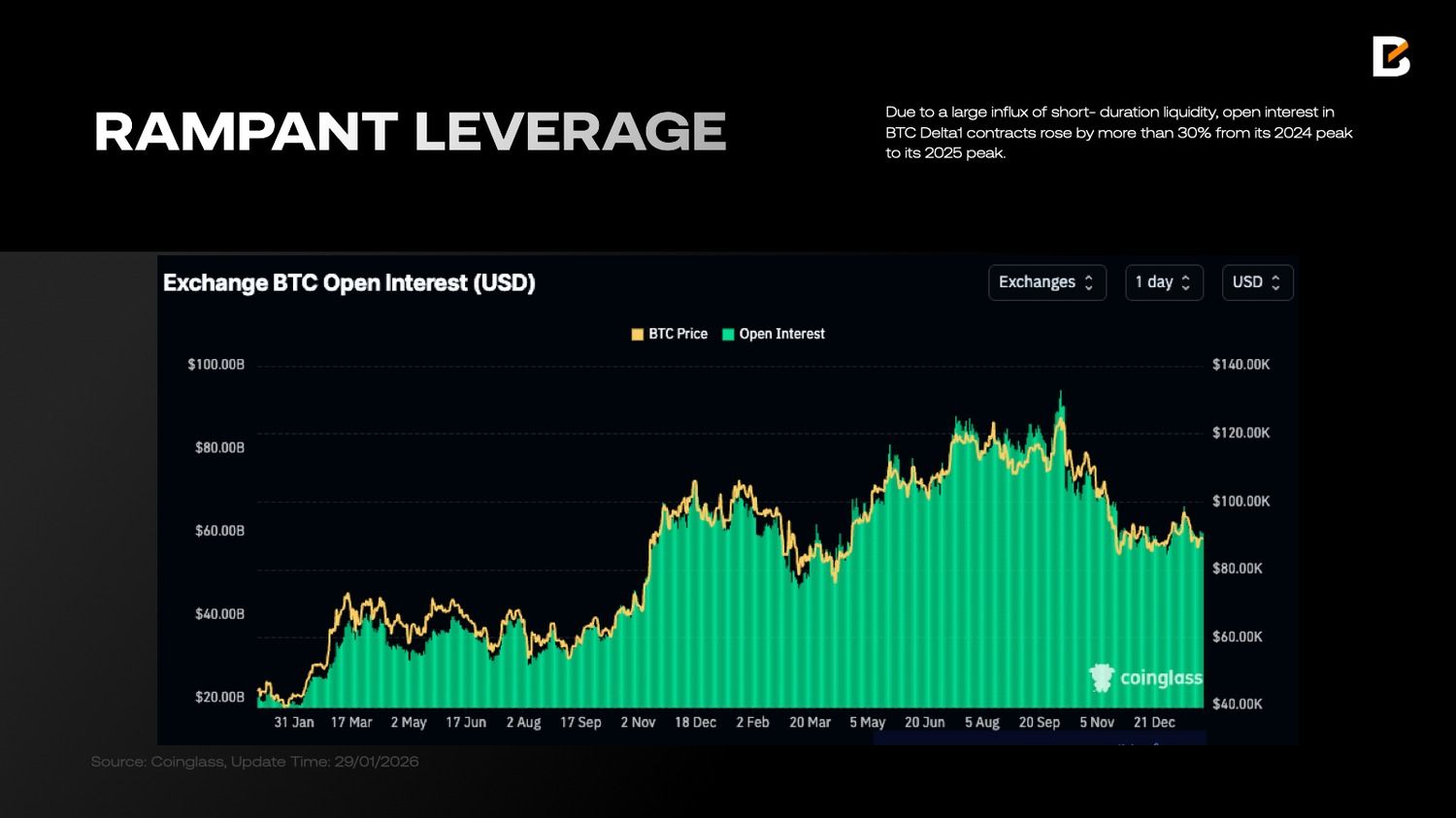

Over the previous yr, business and industrial lending contracted meaningfully versus 2024, and client credit score confirmed comparable weak spot. Against this, VettaFi information recommend that margin debt rose 36.3% over the previous yr, reaching an all-time excessive of $1.23T in December 2025, whereas buyers’ internet debit balances additionally expanded to $ -814.1 billion—broadly matching the tempo of margin debt progress.

As liquidity necessities develop to push markets greater, the banking system is exhibiting indicators of pressure, and demand for short-term funding has elevated. The repair is easy: both scale back margin lending and pull liquidity again, or acquire liquidity assist from the Fed and the repo market.

For the economic system as an entire, the primary possibility is preferable—decrease system-wide leverage and strengthen resilience in banks and the monetary system—however it could additionally indicate decrease valuations and a pointy fairness sell-off. Given the midterm-election backdrop, the White Home is unlikely to just accept that path.

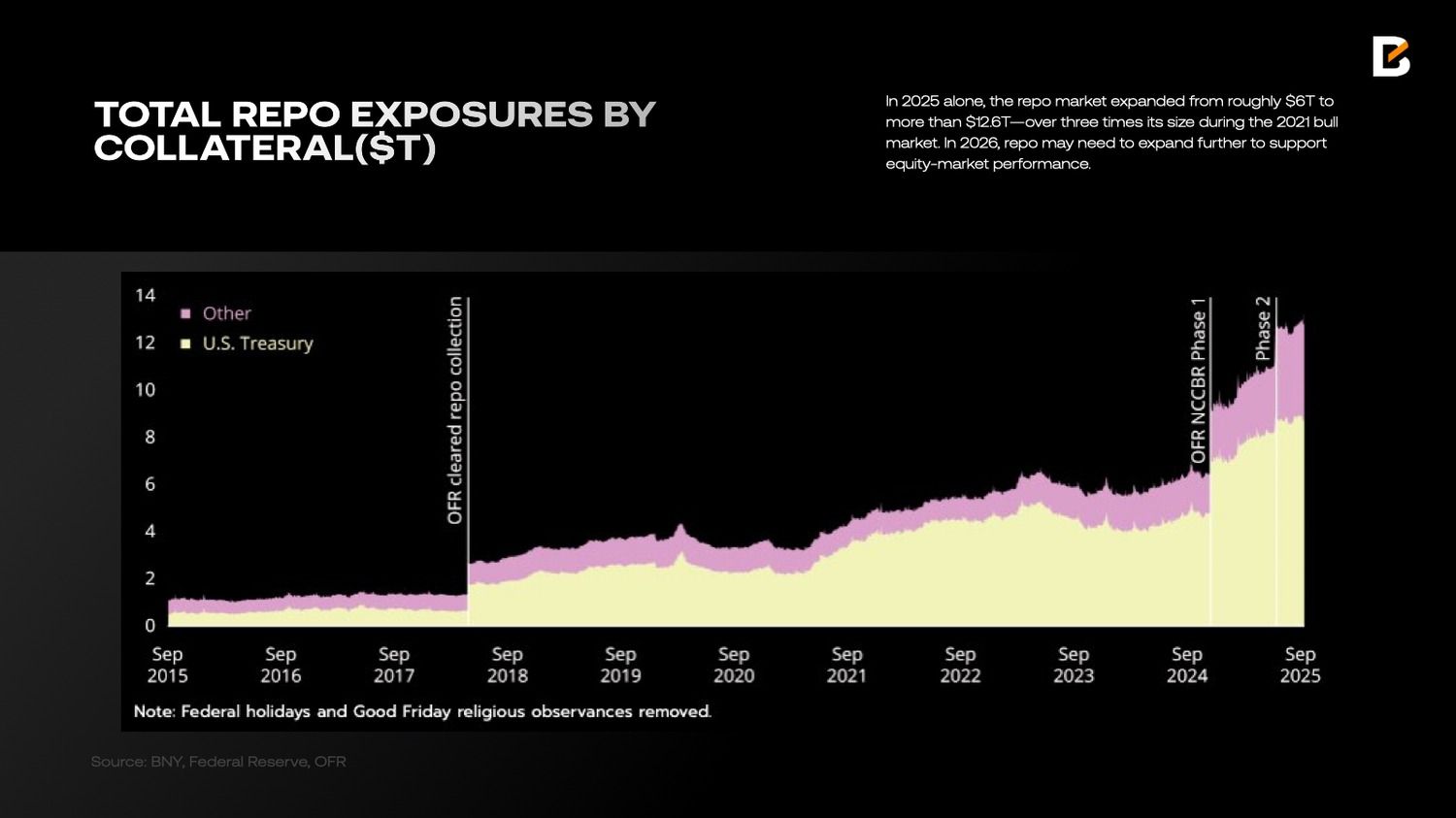

Because of this, in 2025 alone, the repo market expanded from roughly $6T to greater than $12.6T—over 3 times its dimension throughout the 2021 bull market. In 2026, repo might have to increase additional to assist equity-market efficiency.

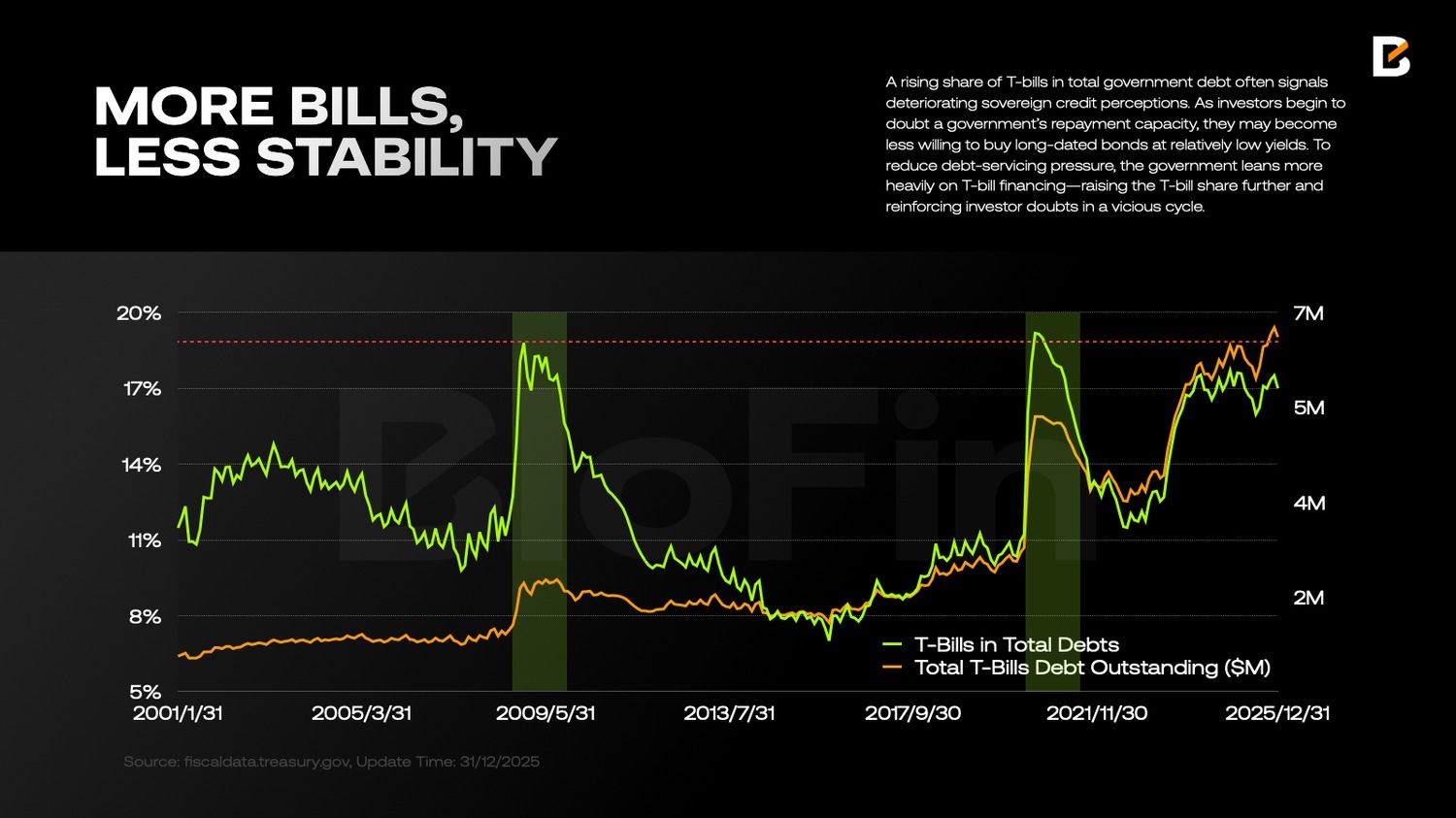

Repo transactions sometimes use US Treasuries—“high-quality property”—as collateral. Traditionally, Treasury notes (T-notes) have been a very powerful type of collateral. However since mid-2023, that has modified, partially as a result of the issuance and excellent inventory of Treasury payments (T-bills) has elevated in an “exponential” trend.

This isn’t benign: a rising share of T-bills in complete authorities debt usually alerts deteriorating sovereign credit score perceptions. As buyers start to doubt a authorities’s reimbursement capability, they could turn into much less prepared to purchase long-dated bonds at comparatively low yields.

To cut back debt-servicing strain, the federal government leans extra closely on T-bill financing—elevating the T-bill share additional and reinforcing investor doubts in a vicious cycle.

A better T-bill share has one other consequence: liquidity dynamics turn into much less steady. Since a big portion of the liquidity supporting equities is channelled through repo, a larger reliance on T-bills implies extra frequent rollovers and a shorter common liquidity “life”.

With total leverage and margin debt already pushing past historic peaks, extra frequent and extra violent liquidity swings weaken the market’s shock-absorption capability—setting the stage for potential cascading liquidations and enormous value strikes.

In brief: the standard of USD liquidity deteriorated markedly in 2025, with no clear signal of enchancment up to now.

So, on this macro context, how have buyers’ expectations and portfolios modified?

Danger Premia and “Strict Diversification”

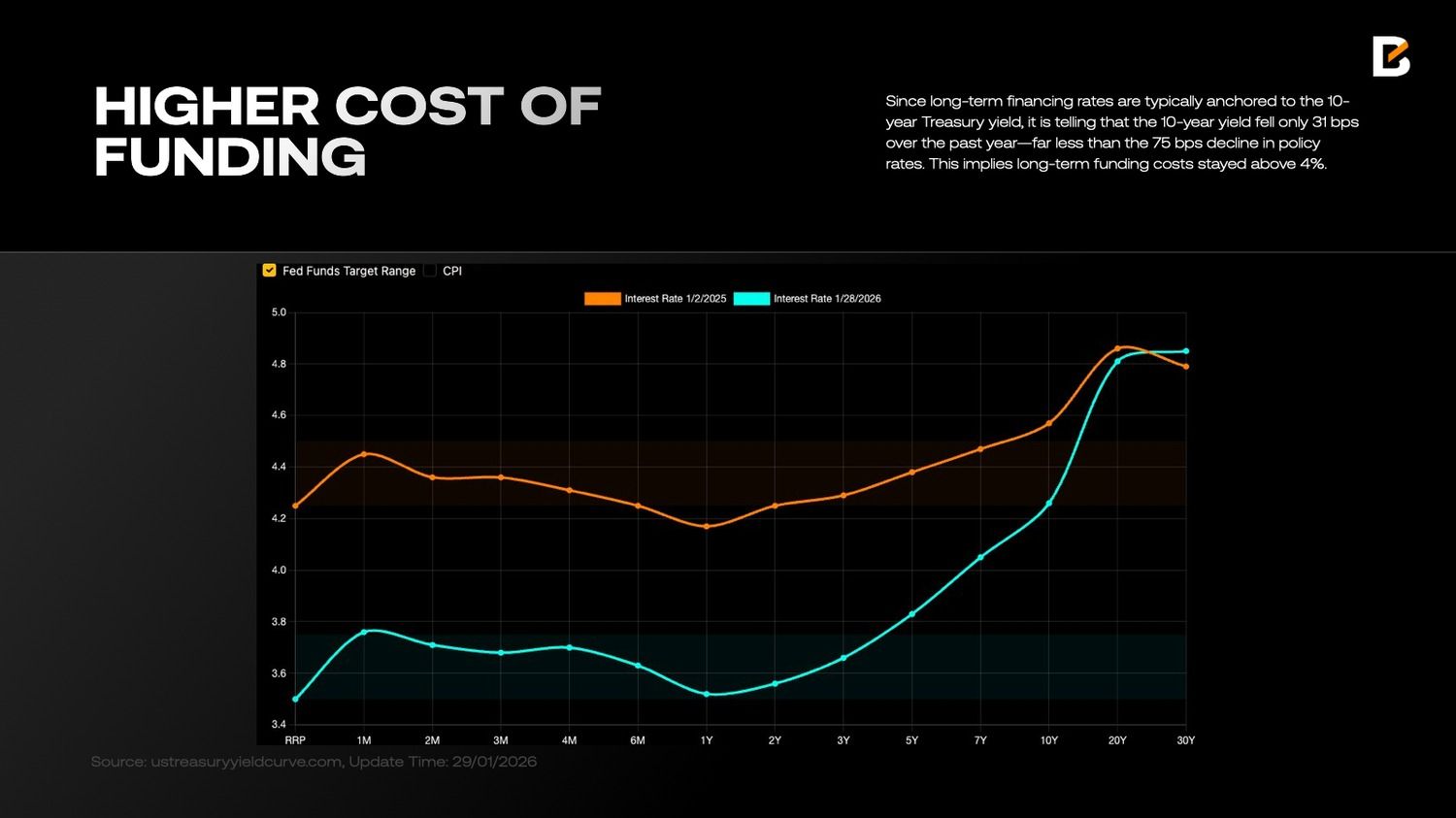

One value of poorer-quality USD liquidity is that USD-based long-term funding prices stay elevated. That is intuitive: as USD asset markets turn into extra fragile, US Treasury debt expands sharply (reaching USD 38.5 trillion by December 2025), and US fiscal, financial and overseas coverage flip extra unsure and fewer predictable, the perceived chance of systemic threat rises over time—prompting long-term Treasury buyers to demand larger compensation.

Since long-term financing charges are sometimes anchored to the 10-year Treasury yield, it’s telling that the 10-year yield fell solely 31 bps over the previous yr—far lower than the 75 bps decline in coverage charges. This means long-term funding prices stayed above 4%.

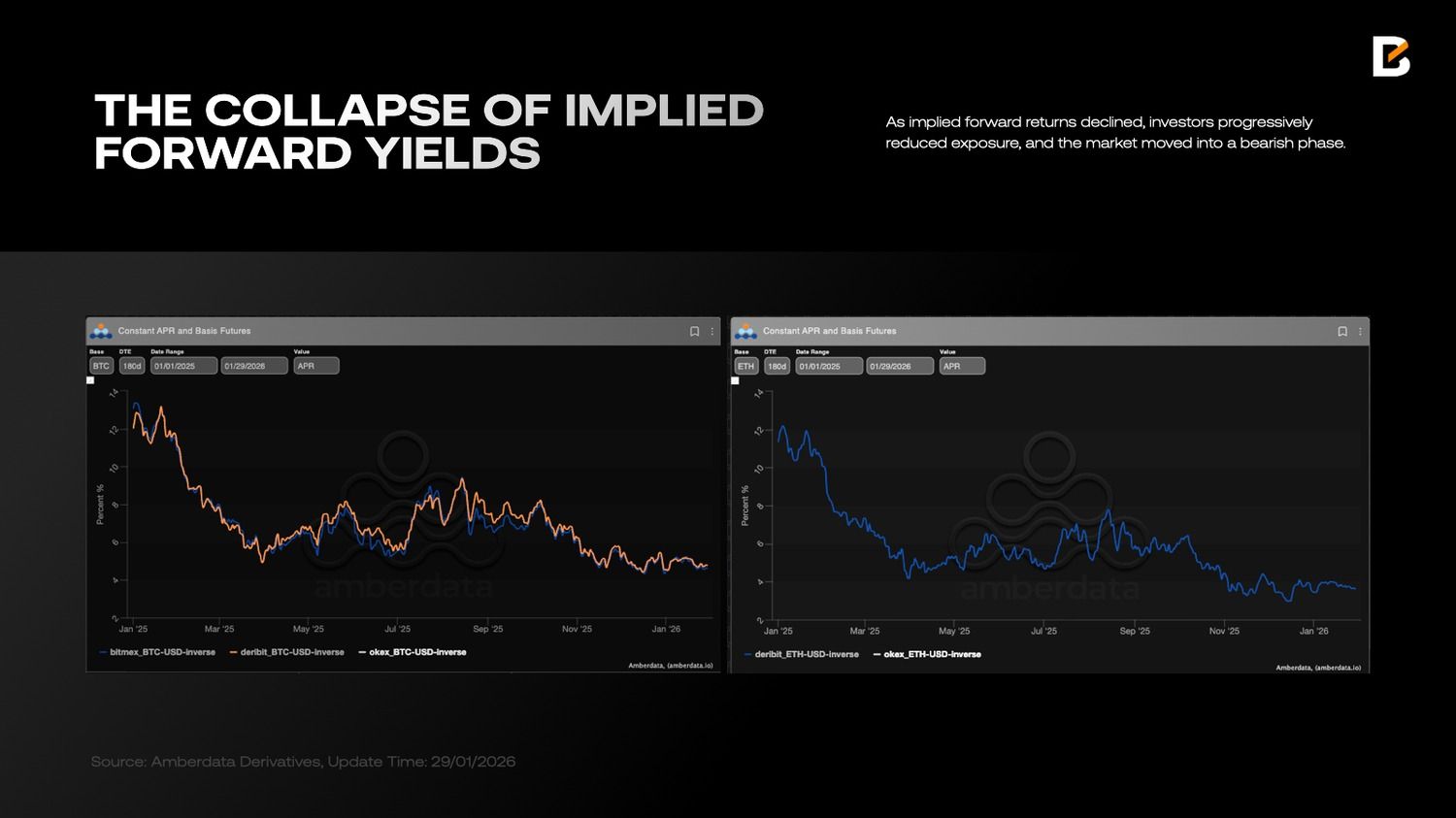

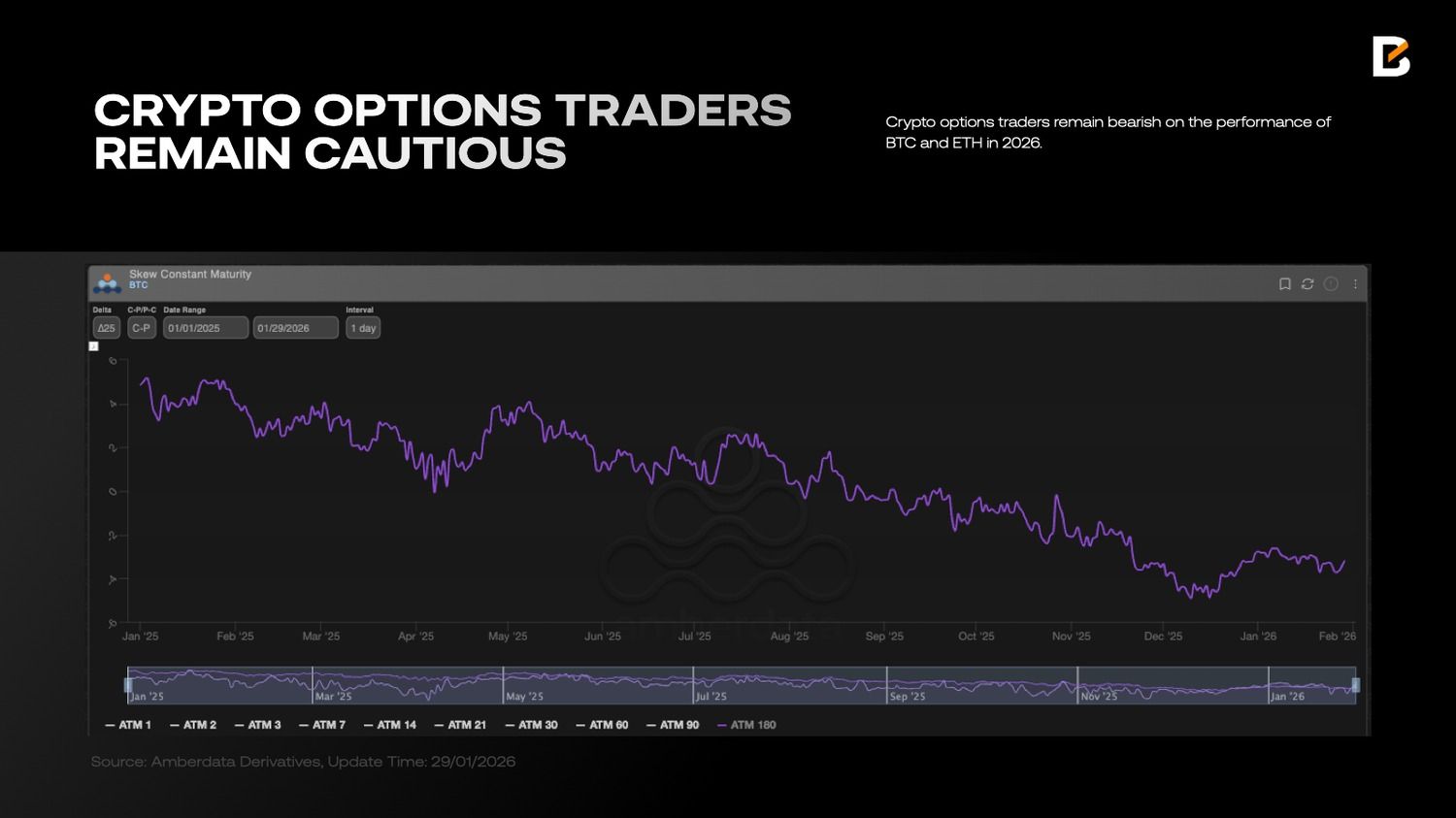

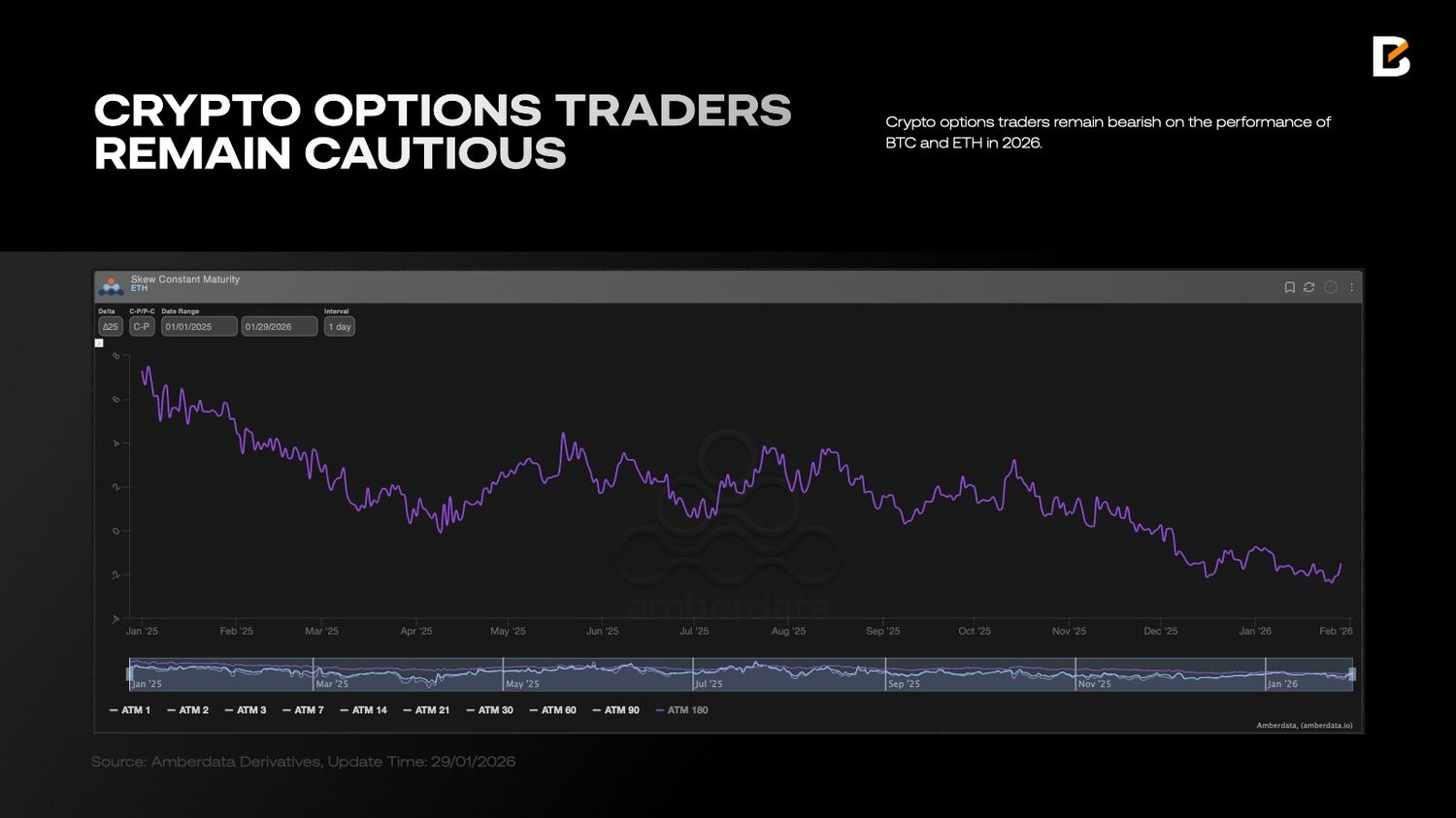

Excessive funding prices constrain positioning. When a threat asset’s implied ahead return falls under Treasury yields, holding that threat asset long-term turns into unattractive. Crypto is a textbook instance: as implied ahead returns declined, buyers progressively diminished publicity, and the market moved right into a bearish section.

In contrast with costly long-term liquidity, short-term liquidity funded through T-bills is materially cheaper. However T-bill funding can be short-duration, creating an surroundings naturally beneficial to hypothesis: buyers can borrow brief, apply excessive leverage, push costs up rapidly and exit. Markets might look buoyant within the brief run, however speculative froth makes rallies troublesome to maintain—one thing clearly seen within the liquidity-sensitive crypto market.

In the meantime, after a long time, “strict diversification” made a comeback in 2025. Not like the normal 60/40 method, liquidity has been unfold throughout a broader set of devices somewhat than confined to USD property.

The truth is, all through 2025, buyers steadily diminished the share of USD and USD-pegged property in portfolios. Though persistent internet outflows didn’t visibly hit US equities, incremental liquidity was allotted extra closely to non-US markets.

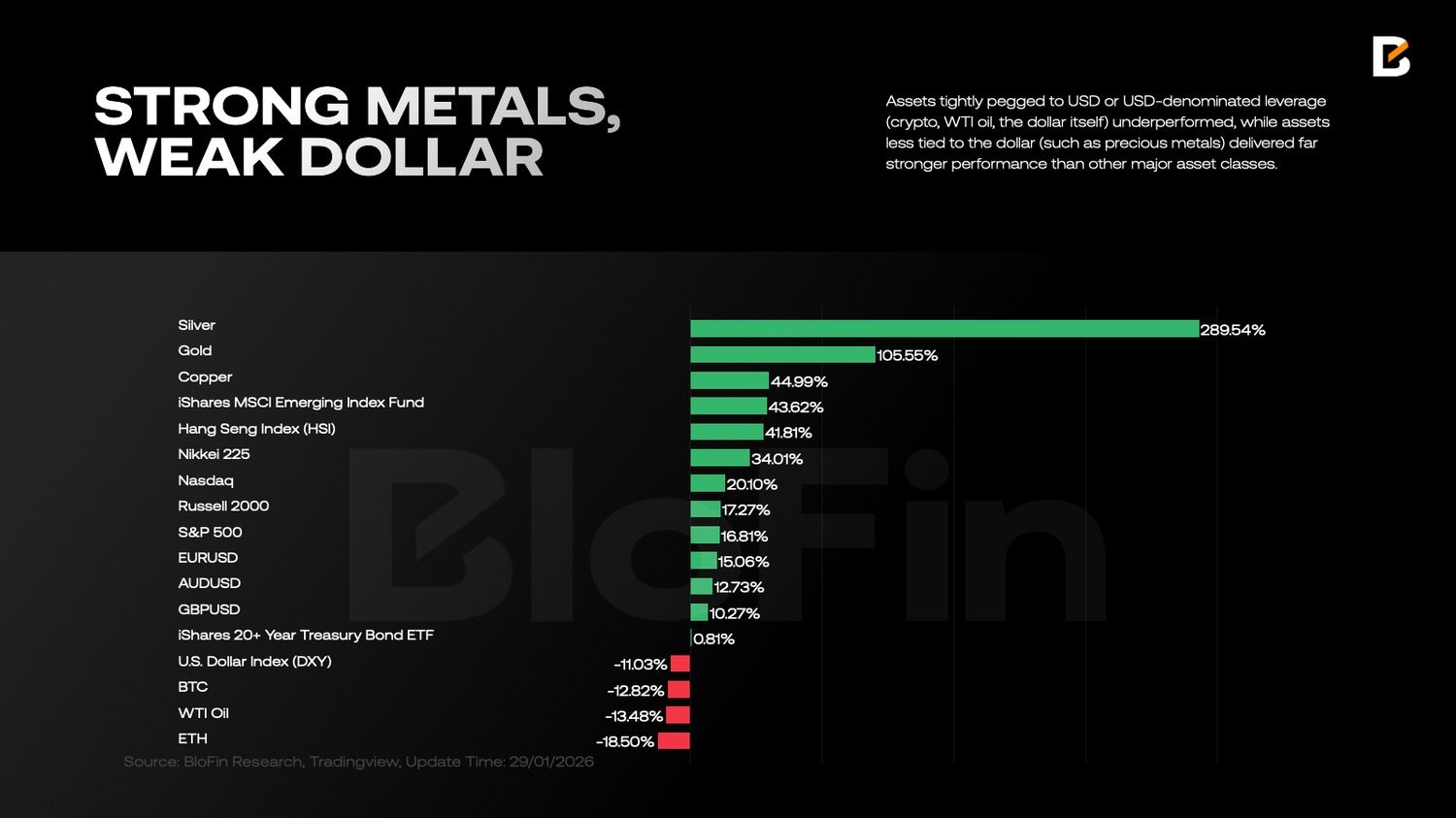

Property tightly pegged to USD or USD-denominated leverage (crypto, WTI oil, the greenback itself) underperformed, whereas property much less tied to the greenback (reminiscent of valuable metals) delivered far stronger efficiency than different main asset courses.

Notably, merely holding euros or Swiss francs carried out no worse than holding the S&P 500. This implies a profound shift in investor logic—one which goes past a single enterprise cycle.

The New Order

What most deserves reassessment in 2026 shouldn’t be a linear query like “will progress be stronger?”, however somewhat the truth that markets are adopting a brand new pricing grammar. Over the previous twenty years, returns usually rested on two implicit assumptions: first, provide chains have been organised round most effectivity, suppressing prices and stabilising inflation; second, central banks supplied highly effective backstops throughout crises, systematically compressing threat premia.

Each assumptions are actually weakening. Provide chains more and more prioritise management and redundancy; fiscal and industrial coverage seems extra regularly in revenue fashions; and geopolitics has shifted from tail threat to fixed noise. “Regionalisation” is much less a slogan than a change within the constraint set going through the worldwide financial system.

On this framework, the bottom line is to not wager on a single course, however to realign exposures to a few extra dependable “arduous variables”: provide constraints, capital expenditure, and policy-driven order stream.

Collectively, they level in the direction of a set of property: commodity-linked equities, the AI infrastructure chain, defence and safety themes, and choose non-US markets that enhance portfolio correlation buildings. On the identical time, the core query in charges and authorities bonds is now not “how a lot tailwind will price cuts carry?”, however how the brand new time period construction reshapes the distribution of returns.

Regionalisation: Not “Decoupling”, however a New Price Operate

Equating “regionalisation” with “full decoupling” tends to understate its true affect. A extra correct description is that globalisation’s goal operate has shifted from “effectivity in any respect prices” to “effectivity below safety constraints”.

As soon as safety turns into a binding constraint, many variables that beforehand sat outdoors valuation fashions—supply-chain redundancy, power safety, entry to essential minerals, export controls on key applied sciences, and the rigidity of defence budgets—start to enter low cost charges and earnings expectations in numerous types.

This produces two direct penalties for asset pricing. First, threat premia turn into much less more likely to revert to structurally low ranges: political and coverage uncertainty turns into an on a regular basis variable, and markets require larger compensation. In any case, no one desires to bear “Cuban fairness threat”, and at present, even in US equities, that “Cuban fairness threat” is now not zero.

Second, international beta explains much less, whereas regional alpha issues extra: below completely different blocs and coverage capabilities, the identical progress and the identical inflation can produce very completely different valuations and capital flows. For allocators, diversification within the age of regionalisation seems to be much less like splitting property evenly by nation and extra like diversifying throughout supply-chain place and coverage elasticity.

Equities: From “Shopping for Development” to “Shopping for Location”

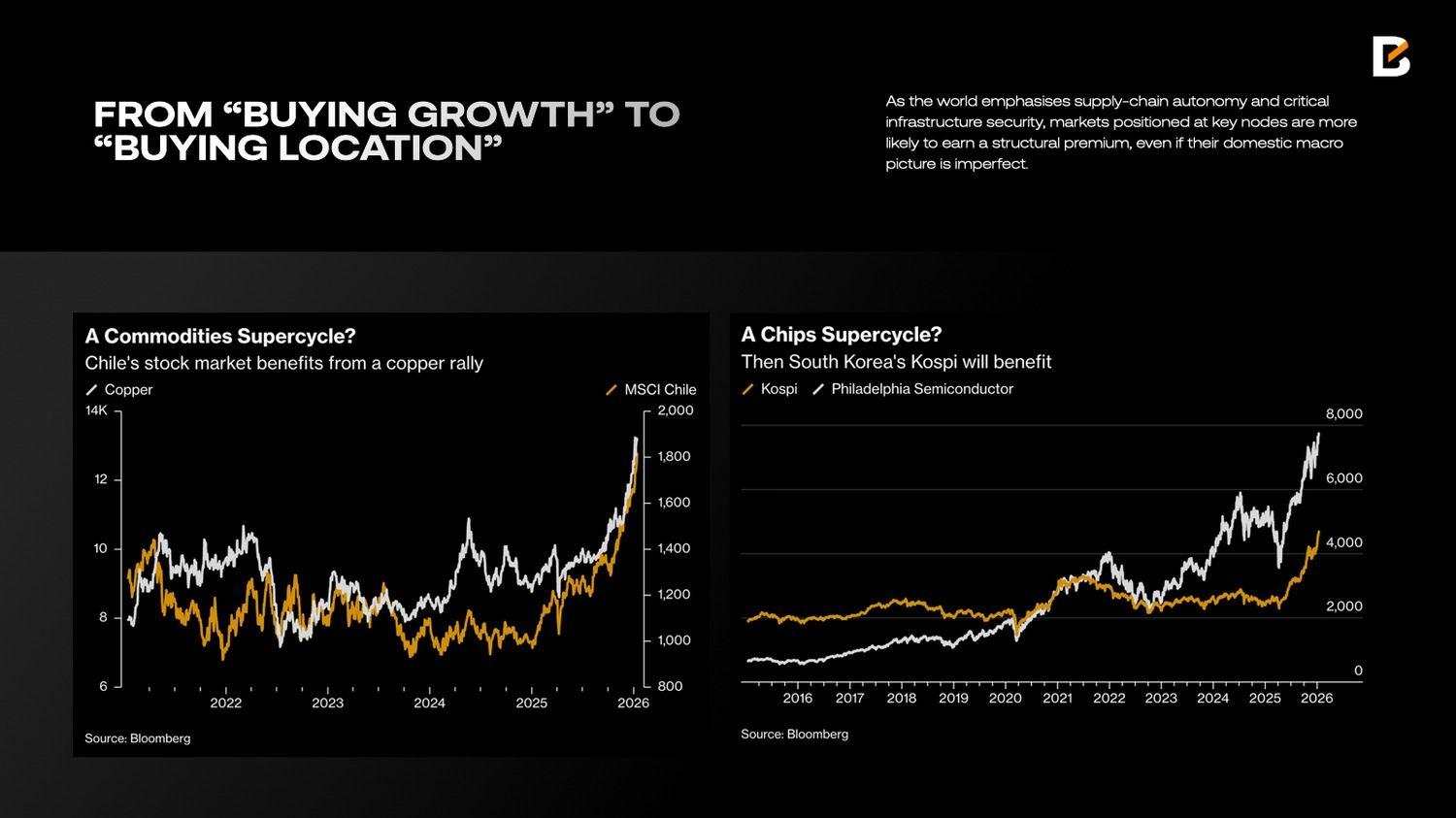

If 2010–2021 fairness allocation was largely about “shopping for progress and falling low cost charges”, 2026 is extra about “shopping for location”. “Location” refers to the place a market sits on three maps: the useful resource map, the compute map and the safety map. Because the world emphasises supply-chain autonomy and important infrastructure safety, markets positioned at key nodes usually tend to earn a structural premium, even when their home macro image is imperfect.

In an period the place safety is the highest precedence, growing inventories of gold, silver, copper and different non-ferrous metals might be rational even when they don’t seem to be instantly wanted. Provide chains might be disrupted with out warning (as final yr’s commerce tensions confirmed), sharply elevating prices and forcing main international locations to carry bigger mineral reserves in opposition to potential shocks.

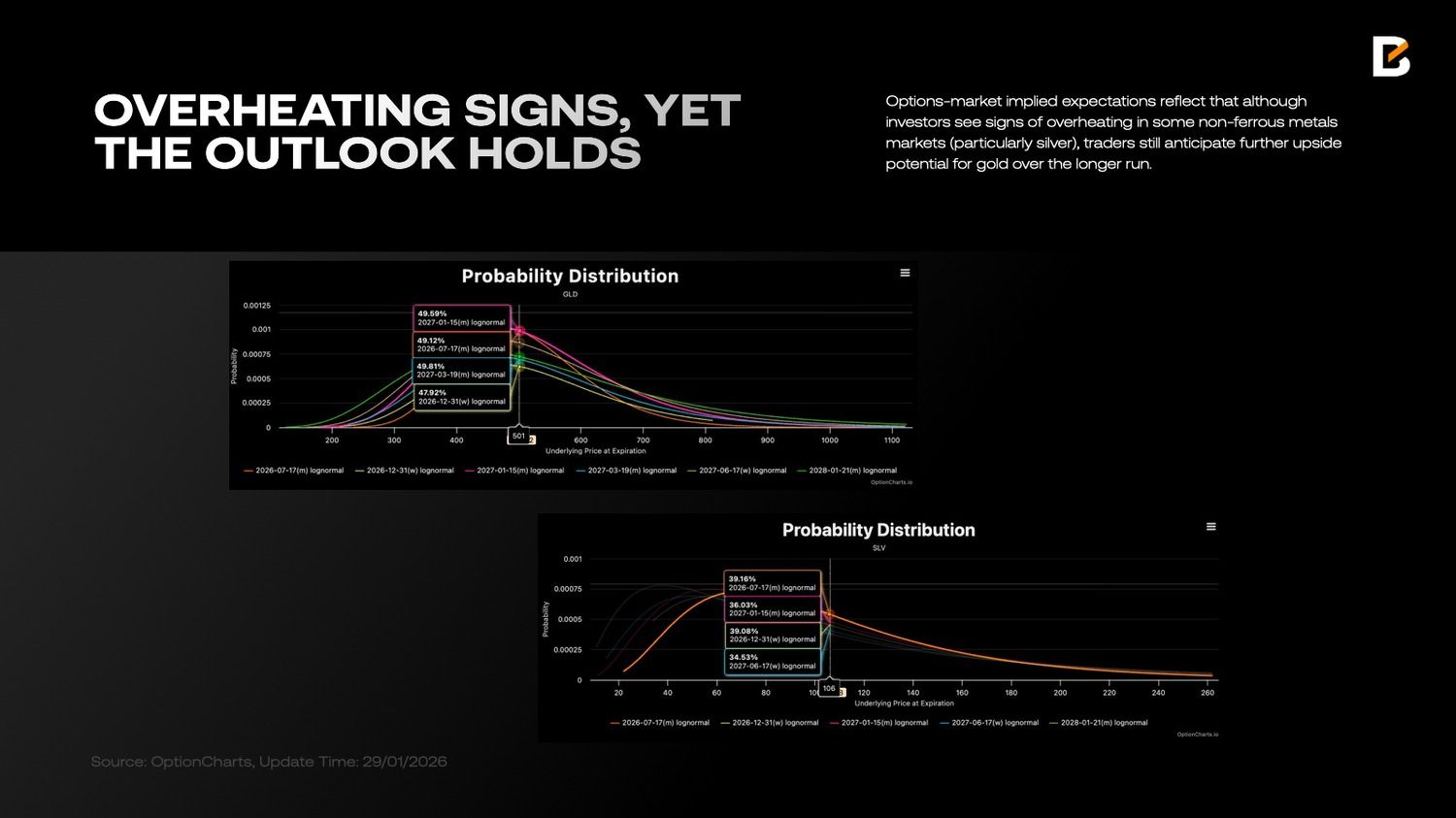

Structurally rising demand for essential minerals, mixed with long-cycle provide constraints, makes commodities behave extra like “supply-side property” than mere mirrors of the normal enterprise cycle. Choices-market implied expectations mirror this: though buyers see indicators of overheating in some non-ferrous metals markets (significantly silver), merchants nonetheless anticipate additional upside potential for gold over the longer run.

This logic additionally supplies a clearer allocation case for equities in resource-rich international locations. Copper-linked equities—Chile is a main instance—partly mirror foundational shifts in electrification and in demand for industrial infrastructure.

Treasured-metals useful resource equities—South Africa is a typical case—mix commodity upside with the double-edged nature of threat premia: when commodities rise, earnings and the foreign money might reinforce one another; when threat rises, politics and exterior financing circumstances can amplify volatility. For portfolio building, resource-country equities are higher understood as a “supply-constraint issue” than merely emerging-market beta.

One other central theme is AI. AI discussions are simply pulled in the direction of application-layer narratives, however allocators ought to give attention to balance-sheet realities: compute, power, information centres, networks, and cooling. These hyperlinks share two traits: greater capex visibility and infrequently profit from joint assist from coverage and trade.

Fairly than treating AI as one other software-valuation recreation, it might be extra sturdy to view it as a brand new wave of infrastructure build-out. Increased compute density in the end interprets into larger energy and engineering demand, shifting extra of the return distribution upstream and into midstream “real-economy” segments.

Below regionalisation, computing infrastructure can be spreading geographically. Increased safety redundancy and localisation necessities enhance the strategic worth of key {hardware} and intermediate items.

Markets reminiscent of Korea, positioned on the industrial interface of worldwide compute infrastructure through semiconductors and important electronics, are sometimes seen as extra direct fairness expressions of the AI capex cycle. For portfolios, the worth of this publicity shouldn’t be solely “sooner progress”, however “extra observable capex and extra steady coverage assist”.

As well as, “defence and safety” has returned to buyers’ agendas for the primary time because the finish of the Chilly Battle. Influenced by Trump’s “Donroeism” and the Russia–Ukraine battle, each the US and Europe are putting defence greater on the precedence record.

The distinctive function of defence property is that demand doesn’t come from marginal family consumption; it’s nearer to a fiscal operate constrained by nationwide safety. As soon as budgets step up, the political resistance to reversing them is bigger, so order visibility is usually stronger. This provides defence-related equities a extra defensive allocation function in a regionalised world: when battle and sanctions threat rise, they’ll add resilience on the portfolio degree.

That stated, defence-sector value sensitivity usually runs forward of fundamentals: event-driven repricing adopted by imply reversion is widespread. A extra sturdy framing is to deal with it as a portfolio “tail insurance coverage” or risk-hedging issue, somewhat than a linear-growth core holding. Its worth lies in lowering drawdowns, not in guaranteeing outperformance each quarter.

Hong Kong equities and mainland China property are one other space price contemplating. Labelling them merely as “low-cost” is inadequate; their allocation worth stems from two components. First, pricing usually bakes in pessimistic expectations early, leaving room for rebalancing.

Second, their coverage operate and sector composition differ from these of US and European property, doubtlessly enhancing portfolio correlation construction. Within the age of regionalisation, correlations don’t mechanically fall; they’ll rise throughout threat occasions. Structurally completely different property can due to this fact present extra significant hedging.

Charges and Treasuries: Hold the Curve Steepening

The core rigidity in 2026 charges markets might be summarised in a single line: the entrance finish is extra a operate of the coverage path, whereas the lengthy finish is extra a container for time period premia.

Price-cut expectations do assist front-end yields decline, however whether or not the lengthy finish follows is dependent upon whether or not inflation tail dangers, fiscal provide strain and political uncertainty enable time period premia to maintain compressing. In different phrases, long-end “stubbornness” might not imply markets have mispriced the variety of cuts; it might imply markets are repricing long-run threat.

Provide dynamics amplify this structural distinction. Modifications in US fiscal funding composition immediately have an effect on provide–demand throughout maturities: the entrance finish is simpler to soak up when cash markets have capability. In distinction, the lengthy finish is extra liable to pulse-like volatility pushed by threat budgets and time period premia.

The portfolio implication is evident: length publicity must be managed in layers, avoiding a one-path wager on “inflation absolutely disappearing and time period premia returning to ultra-low ranges”. Curve-structure trades (as an example, steepening methods) persist not merely due to superior buying and selling talent, but additionally as a result of they align with the completely different pricing mechanisms of the entrance and lengthy ends.

Crypto: Separate Accounting for “Digital Commodities” and Secondary Danger Property

In 2026, the important thing for crypto shouldn’t be merely “will it rise?”, however sharper inside differentiation. Bitcoin is extra readily understood as a non-sovereign, rules-based provide asset that’s moveable throughout borders—a “digital commodity”. Below a regionalisation narrative, it’s extra more likely to soak up demand for various fee methods and hedges.

Against this, a subset of tokens that behave extra like equity-style threat property are priced extra on progress tales, ecosystem growth and threat urge for food. When risk-free yields stay engaging, regulation turns into clearer, and conventional capital markets provide extra mature funding and exit channels, equity-like tokens should provide greater threat compensation to justify allocation.

Because of this, crypto allocation is healthier approached through “separate books” somewhat than a single basket: place bitcoin in a commodity/alternative-asset framework, utilizing small weights to acquire portfolio-level convexity; deal with equity-like tokens as high-volatility threat property with stricter return hurdles and clearer threat budgets. The core of the regionalisation period is to not embrace each new asset, however to establish which property stay extra explainable below the brand new constraints.

Use Onerous-Constraint Property because the Core, Use Structural Divergence because the Return Engine

Placing the above collectively, a 2026 portfolio seems to be extra like managing a set of “arduous constraints”: provide constraints restore the strategic function of commodities and useful resource equities; capex helps earnings visibility throughout the AI infrastructure chain; policy-driven orders improve the resilience of defence and safety; the return of time period premia reshapes the distribution of length returns; and choose non-US property present reflexive hedging via valuation construction and coverage capabilities.

This doesn’t require excellent prediction of each occasion. Quite the opposite, the rarest talent within the age of regionalisation is to put the portfolio ready that depends much less on flawless forecasting: let arduous property and infrastructure soak up structural demand; let curve buildings soak up structural divergence; and let hedging components soak up structural noise.

Buying and selling in 2026 is now not about “guessing the reply”, however about “acknowledging constraints”—and rewriting asset-allocation priorities accordingly.

Disclaimer: The data supplied herein doesn’t represent funding recommendation, monetary recommendation, buying and selling recommendation, or every other kind of recommendation, and shouldn’t be handled as such. All content material set out under is for informational functions solely.